The corrugated industry’s benchmark containerboard prices should reflect underlying market conditions, but Green Markets finds that the two appear to have diverged in the past three months.

In February, there was no movement among buyers and sellers we contacted, yet the benchmark publication lowered prices by $20 a ton. In March, we reduced our assessment by $40, reflecting consistent reports of lower transaction prices, which might have reflected undisclosed declines from late 2025. The same month, the benchmark raised prices by $40. In April, it moved higher again, by $30, while we observed little to no change.

Something isn’t lining up. The mechanism used to signal price movements looks increasingly detached from where business is being transacted, particularly in the independent market.

The March prices for kraft linerboard disclosed to us by independent buyers ranged from $660 to $760 a ton—well below the benchmark’s $995 a ton. We may be looking at different data or asking different questions; either way, the gap is too large to ignore.

With most box pricing still tied to the benchmark, that gap can shape the perception of cost increases as they move through the system. A $50-a-ton hike is roughly 5%, based on the benchmark, but for independents buying around $700 a ton, it’s 7% or more.

For integrated producers, higher paper prices can be largely circular. The mill sells to the box plant, the box plant sells to the customer, and margin can be preserved—or enhanced—depending on how much of the increase sticks. Raising box prices even 1% is immediately additive.

Independents lack that flexibility. Recovering rising paper costs requires raising box prices. Yet demand is soft, and competition is intense in this market, with box buyers seeking price relief through requests for quote.

The nominal price difference may be absorbed through delayed pass-throughs, selective rebates, or transactions at below-market levels. But if the published price continues to rise as deals lag behind, the benchmark risks becoming less a reflection of the market and more an aspiration for it.

That’s a fragile position for a system that underpins a large share of contracts across the industry. As we’ve noted before, the index is built on a relatively small pool of transactions and can struggle to capture broader dynamics.

What integrated producers can’t do—at least not for long—is push paper prices higher while competing aggressively on box pricing. That strategy always tends to end the same way: margin compression, customer pushback, and another round of resets.

Higher Costs Are Real

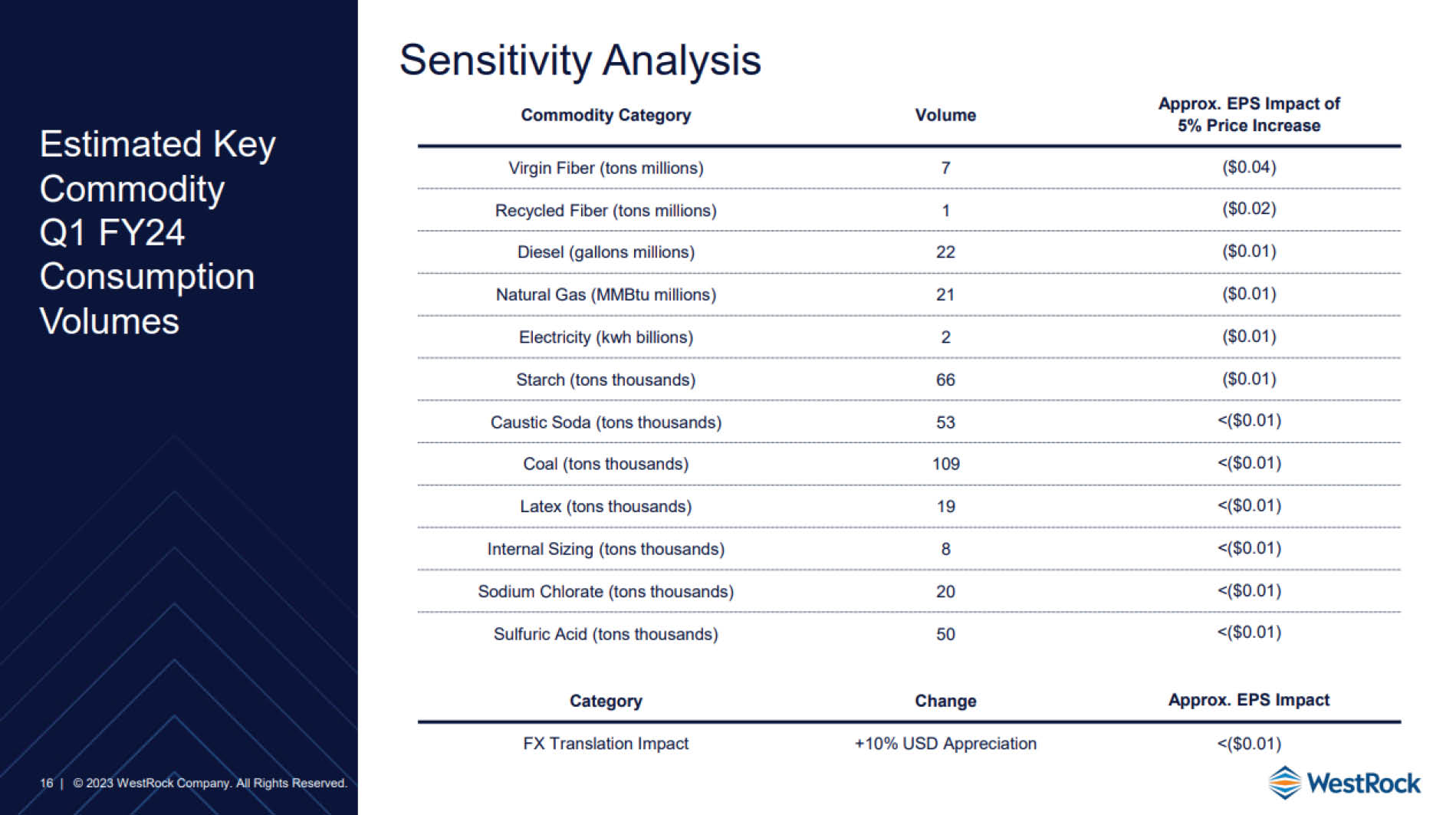

Fuel is the most visible driver of the corrugated industry’s recent cost increases. Diesel prices are up roughly 40% from earlier this year, creating a meaningful drag on earnings. WestRock, for example, consumed about 22 million gallons of diesel per quarter in 2023. At current levels, that implies roughly $30 million or more in additional quarterly fuel costs.

The increases don’t stop at the pump; they flow directly into recovered fiber. Old corrugated container (OCC) benchmarks, much like containerboard, often fall short of capturing what buyers actually pay. The index may reflect a free-on-board price but not the cost to move material to the mill. With both OCC and diesel prices rising, the true landed cost has moved higher than the headline numbers suggest.

Other inputs are more mixed. Natural gas spiked earlier in the year but has since retreated and now sits below its trailing 12-month average. Electricity, however, continues to trend higher, driven by inflation, grid investment, and growing demand from data centers and electrification. Some producers are responding by investing in on-site generation, with Packaging Corp. of America moving to install gas turbines at selected mills.

Labor-related costs are also moving in one direction. Medical benefits continue to climb, with employer-sponsored family premiums approaching $27,000 in 2025 and expected to rise again next year. Higher utilization, rising hospital pricing, and the adoption of newer therapies are all contributing to the increase.

Ryan Foxis a corrugated market analyst at Green Markets, a Bloomberg company. He can be reached atrfox93@bloomberg.net.