July 3, 2024

-

- Take an active role in defining contribution and do not leave it up to the software consultant (you all know that my view of the word is to simply use material margin).

-

- Keep your general ledger buckets pure by not comingling costs.

-

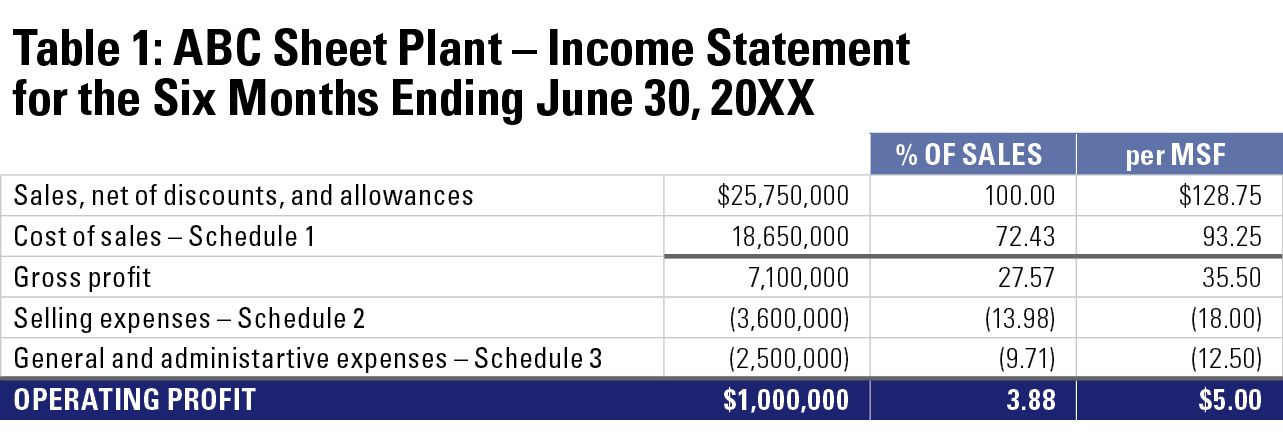

- Put your financial statements into “estimating system format” at least down to the contribution line.

-

- Define and create meaningful cost centers to help you understand and manage your business.

-

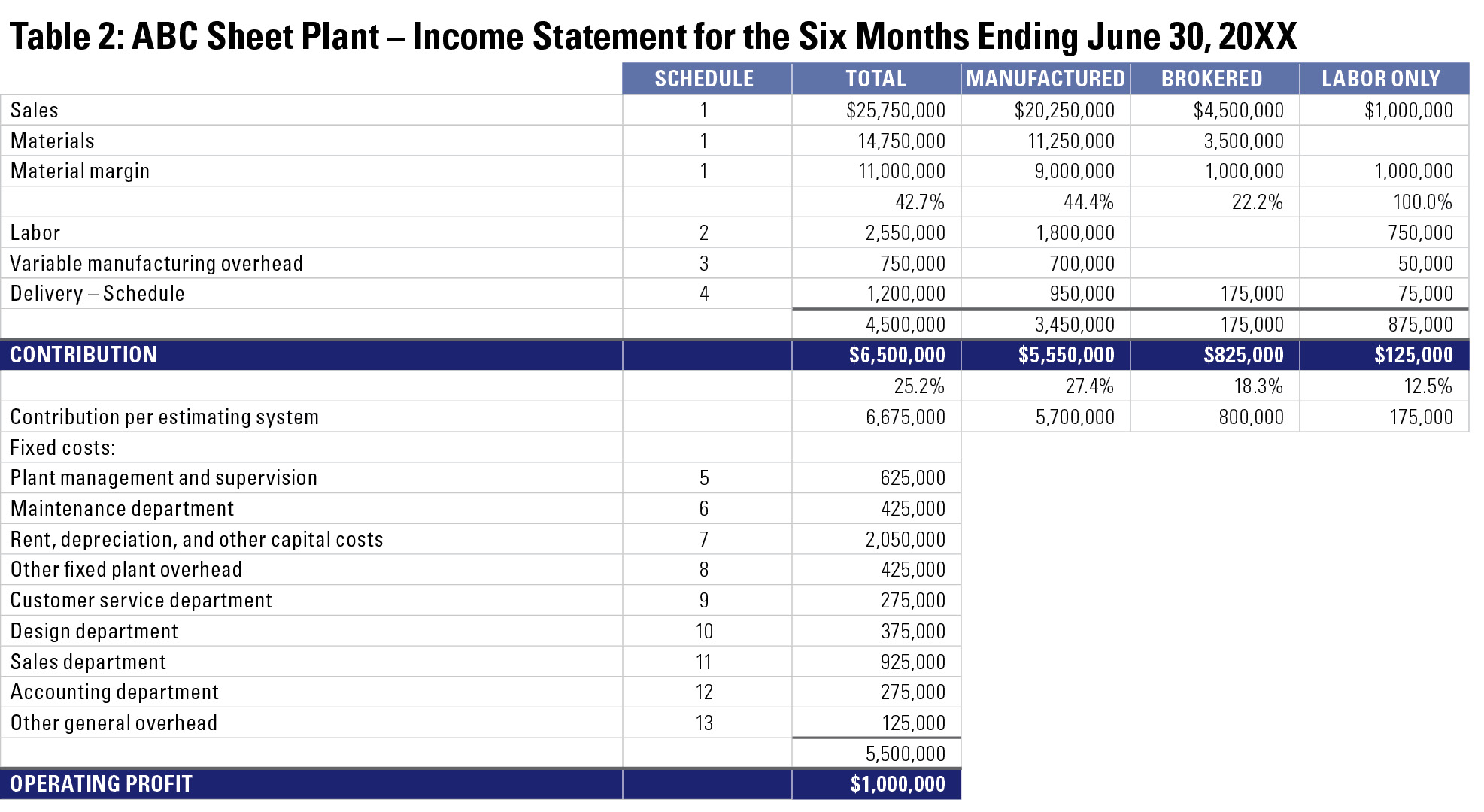

- Separate manufactured from nonmanufactured goods and their related activities on your income statement.

-

- Define and create profit centers within the various manufactured and nonmanufactured goods categories, and track profitability within them.

-

- Keep the face of the income statement clean, and utilize subschedules to add details.

-

- Add nontraditional performance metrics to include color and analytics to your results.

-

- Facilitate reconciliations between actual and estimated results. While you may currently be able to do a “big picture” reconciliation of contribution between actual and estimated results, it is almost impossible for you to tie in any of the details. Understanding where you are making the highest margins and comparing that data with where your estimating system thinks you are making the highest margins is just about the most important information that a converter can have at their disposal.

-

- Ability to understand the profits generated by various business segments. While converting paper into packaging will always be at the core of what you do, most independents tend to focus on value-added and niche business because that cannot compete with the low-cost structure of larger mill-based companies.

-

- Gain a greater understanding of the costs of various endeavors. If you don’t report on departments in any meaningful way, it is almost impossible to know what they really cost.

-

- Looking at expenses on a percentage-of-sales basis can often lead you to the wrong conclusion because the higher the sales price, the lower the cost looks as a percent of the sale. Two companies with a similar-sized plant, workforce, and equipment could have the same dollar cost of a particular expense, but on the books of the company with the higher sales price, the expense will have a lower percentage of sales. This is why many companies like to express their costs as a function of the footage shipped. The problem with this is that from a manufacturing perspective, what matters is footage produced. You can have a high production month, when a lot of the goods produced get shipped in the following month, so looking at expenses solely on the basis of footage shipped can yield flawed data.