November 5, 2025

Unless there is a paradigm shift in American politics, which is always possible, we have entered into a tax and business climate that is quite favorable for the closely held independent converter.

Tax rates for C corporations are permanently fixed at 21% and for pass-through entities at 29.6%. Deductibility for research costs and interest expense have been largely restored. One-hundred percent bonus depreciation has now been made permanent, making the climate for purchasing equipment more favorable. The estate tax exemption has been increased to $15 million and is indexed for inflation, so a husband and wife can pass $30 million in assets to their heirs, making it much easier for families to protect the wealth they have accumulated. We also have an administration that is committed to imposing far fewer regulations on businesses, thus reducing the costs of operating.

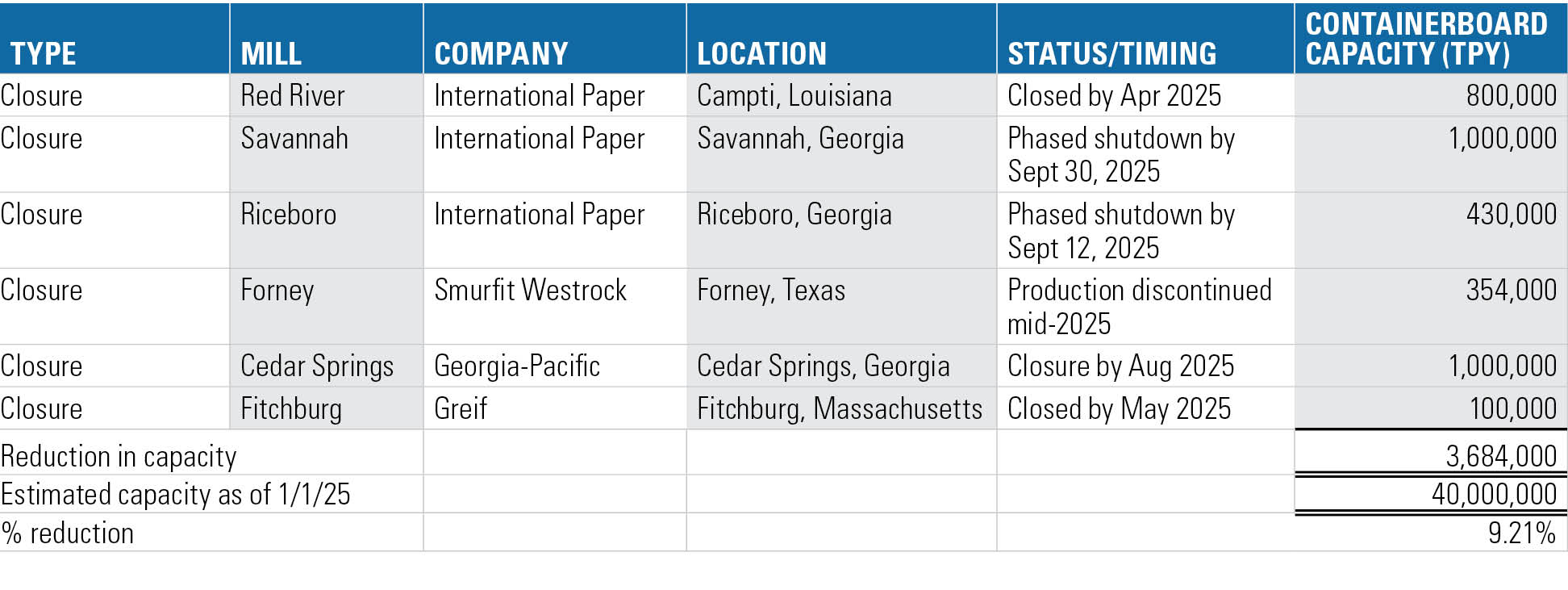

Paper companies are focused on the imbalance of supply and demand in the containerboard markets and are closing mills at never-before-seen rates. Per the chart below, a staggering 3.68 million tons of production will be taken out of the market this year. There are about 825,000 tons of capacity expected to enter the market over the next two years, so the net reduction equals roughly 7% of the total marketplace.

The chart also highlights the shift of the marketplace to lighter-weight recycled grades of paper, as all of the projected new capacity is going to produce recycled paper, and almost all of the mills that closed produced virgin paper. Fastmarkets RISI suggests that recycled linerboard sells for $100 per ton less than virgin, while Bloomberg and others suggest that the discount is larger. In any event, specifying lighter-weight recycled paper combinations in the board that they utilize may allow independents to offer their customers more competitive profits and higher profit margins.

There has been little to no growth in corrugated box shipments since the end of the COVID-19 pandemic, and in point of fact, Fastmakets RISI has reported that corrugated shipments are down 2.1% year over year in the first quarter of 2025 and predicts a 1.9% decline for the full year. Despite this, there have been several increases in the reported price of containerboard, so the mill closures should go a long way toward shoring up prices. In my travels over the past 35 years, I have seen independents generally pick up margin when the price of containerboard goes up and often lose margin when the price of containerboard goes down. This makes the mill closures and the expected effect on containerboard prices even more welcome.

The converting business has fundamentally changed over the past 30 years. While it was always somewhat capital- and labor-intensive, the cost of both has risen significantly. When I first got involved in the business, I vividly remember a client who had a few million dollars in sales and went out and bought an old flexo for $50,000, set up shop in an abandoned bowling alley, and was profitable in his third month of operations. Those days are long gone. We now live in an era of automatic case erectors and a need for making our packaging to precise tolerances.

Printing is also being held up to very high standards, and inside and outside printing is becoming more the norm than the exception. Labor rates are at an all-time high and the price of benefits is enormous, while at the same time the labor pool for plant labor has been problematic, although it does show some signs of improvement. Similarly, the price of ancillary equipment, such as CAD tables, ink kitchens, and plate and die storage, runs into millions of dollars. Software systems and solutions for things such as order processing, graphic and structural design, and plant reporting and efficiencies are more sophisticated and significantly more expensive.

The capital costs of starting a modern sheet plant without taking into account real estate can be in excess of $20 million and a full-blown corrugator plant in excess of $35 million, depending on how much new equipment is purchased, how much conveyor is required, etc. The cost of industrial real estate has almost doubled in the last 10 years, whether owned or rented. Although this seems to be stabilizing somewhat of late, the days of leasing space for $2 per square foot are long gone. All of these costs, in conjunction with startup and other soft costs, create a significant barrier to entry into this marketplace.

With all of this said, new plants are being built, but most of them are being built by integrated companies and some of the larger independent converters in order for them to stay competitive with their integrated brethren. No one really knows how much of the marketplace belongs to independent converters versus integrated companies, but no matter how sophisticated the integrated converting plants become, there will always be a need for the independent sector to handle shorter orders that go across multiple machines that require fast turnaround or managed inventory levels. There has also been tremendous consolidation among the independents, and the ones that are left are for the most part larger and better capitalized. In 1990, there were 25 independent corrugators in the New York area alone; today there are three and not that many sheet plants either. The same kind of consolidation can be said about Chicago, Los Angeles, Atlanta, and just about every other major city in the country.

I think that we are on the cusp of a golden age for the independent converter. The climate for taxation and government regulation is favorable. The containerboard producers are making the moves necessary to foster future price increases, which should be good for independents. There are significant barriers to entry into the marketplace, and though overall demand has been sluggish, there will always be a need for the kind of innovative and customer-oriented packaging that the independent converter provides. Interest rates are coming down, which will help reduce capital costs and improve operating margins.

There is, however, some significant uncertainty about the effect of tariffs on the marketplace, and some kind of a recession may be in our near future. So while I am optimistic about the long-term future of the independent converter, this may not be the time to take on additional risk. My advice for all of you is to come up with a long-term plan to work your niches and to develop new ones, to continue to become more efficient in your plants, and to look for good deals on equipment purchases and upgrades. In my opinion, this plan should include taking steps to learn how to convert lighter-weight recycled paper. Major European producers such as Smurfit Kappa and DS Smith are here, and their European customers have long embraced this change. All of the newer mills coming online have the capacity to manufacture lighter-weight recycled board, so this will become an increasingly important part of your future. My advice is to come up with a plan to embrace, rather than resist, this trend.

Tariffs and the weaker dollar have raised the cost of equipment significantly, since so little of it is produced in the United States, but 100% bonus depreciation is here to stay, so there is no rush to maximize your tax position. This is the time to pay down debt and build up capital reserves and plan your long-term future, while at the same time you should (always) have a plan in place to deal with a temporary economic downturn. The failure to plan is usually a plan to fail, and this would be a good time to go into “planning mode” and make sure you make the right decisions to maximize your long-term profitability.

Mitch Klingher is owner of Klingher Nadler LLP. He can be reached at 201-731-3025 or

mitch@klinghernadler.com.