March 20, 2024

A few years ago, the cadence of the corrugated industry’s production data changed. Instead of being published monthly, it started showing up quarterly—and with a lag. It’s not clear why. Maybe box plants were taking too long to report their numbers, or the industry wanted to shield containerboard prices from declines in mill operating rates. Or perhaps the delay was intended to protect publicly traded producers from shortsighted investors. Whatever the reason, the industry became opaquer, at least to outsiders.

This lack of transparency prompted Green Markets to begin reporting on the industry almost four years ago. Corrugated packaging’s reach makes it a potential bellwether for the broader economy. Yet sources of market information are limited, with all box contracts tied to benchmark containerboard prices published by a single provider. In April 2020, as the COVID-19 pandemic settled in, we began calling box plants to find out what was really happening.

By 2021, we had developed a network of industry contacts. As I told one box plant owner, “You are currently a lot like Washington, D.C.—taxation without representation. I’m here to offer you a voice and to tell your side of the story.” As it turns out, a lot of independent box plants wanted to share their stories.

These conversations included sentiments about future demand. By asking dozens of industry participants each month how they feel about box demand, we avoid company-specific information and get a broader sense of how the market’s shaping up. Box producers give their opinions on prospects for the next month and three months in the future, and the responses go into a spreadsheet. Comparing them across time allows us to catch the most compelling data—when feelings change.

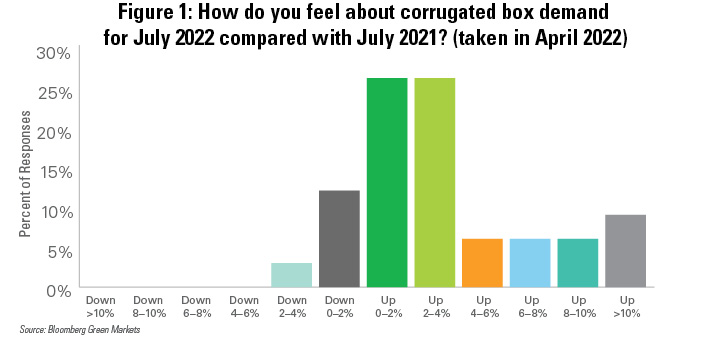

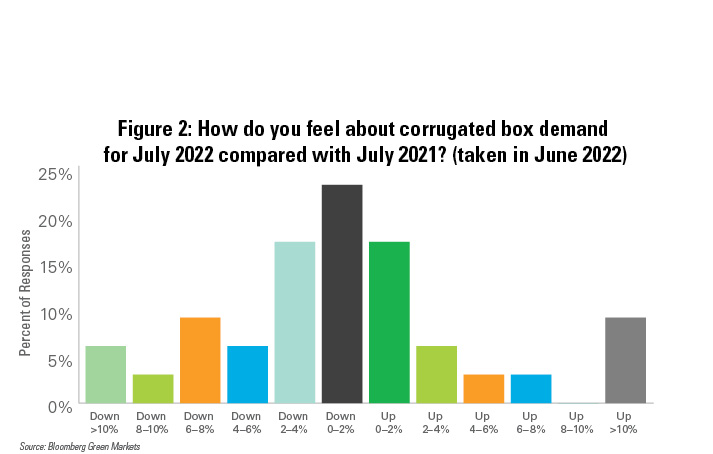

In April 2022, for example, we asked about expectations for demand three months ahead in July, and the outlook was mostly positive (Figure 1). That June, we polled producers again about July, and the overall result was surprising: a 5 percentage point negative swing in the outlook (Figure 2). Industry shipments ended up falling 8%. June’s sentiment data had warned of the downturn a month before it happened.

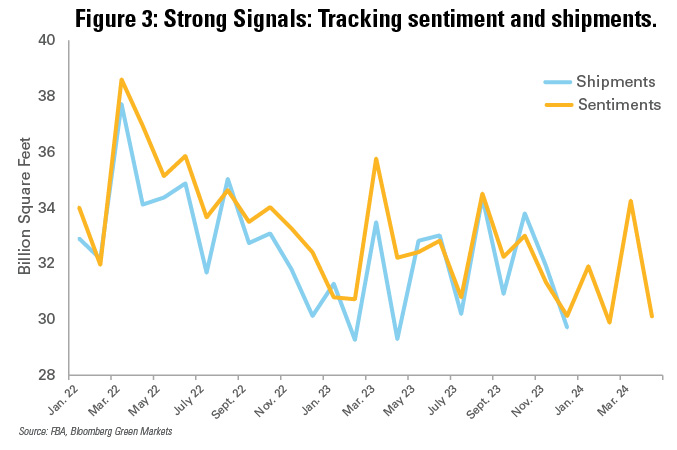

Green Markets’ sentiment samplings now have a two-year track record. On average, our figures tend to be up to 260 basis points too optimistic. If sentiments indicate that box demand could increase 2.6% next month, there’s a good chance shipments will come in flat to up 2.6% year over year. The chart on page 8 shows the gaps between the two.

In November, the industry outlook for 2024 appeared a bit bearish to us. Based on forecasts from brands and retailers, we expected box volume to be down about 1% this year. So far, box plant sentiments are pointing in the opposite direction, showing a first quarter improvement of about 2% from a year earlier. If our normal optimism error holds, the quarter may still be flat. Yet U.S. consumers don’t appear to be done spending, and even manufacturing is showing signs of strength, with the January new orders index at 52.4.

Green Markets’ sentiment metrics can’t specify the level of future demand, but they can signal how it’s trending if we can take the temperature of enough box plants. Having more participants in the process would help us offer more accurate and detailed insights from boxmakers, whose views are important to everyone in the industry. After all, they sit on the front lines, closest to end users. They may not care about what paper mills are doing, but mills should be aware of what box plants are seeing in the market.

Ryan Fox is a corrugated market analyst at Green Markets, a Bloomberg company.