May 11, 2026

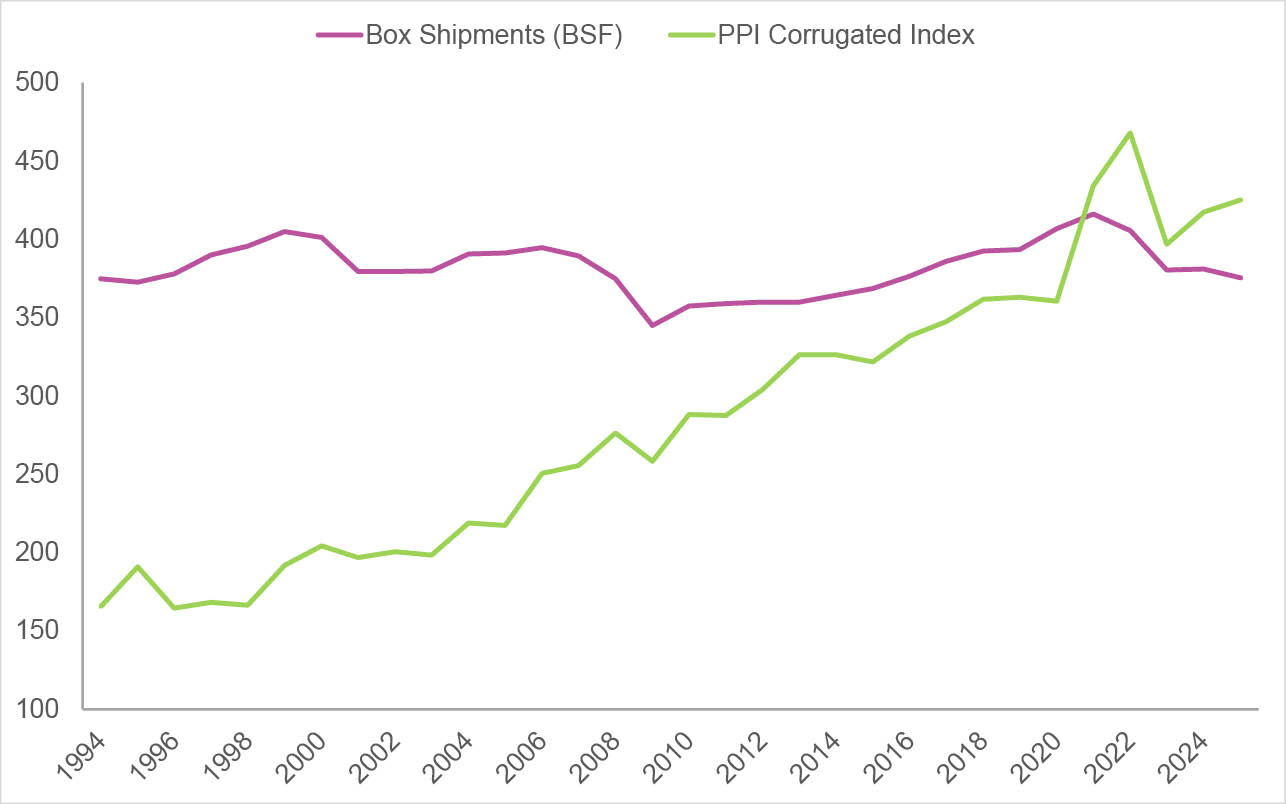

Prices don’t always fall when demand declines. In mature, highly competitive industries such as U.S. corrugated packaging, tonnage can drift lower, square feet of box shipments can slide, and prices can still rise. This isn’t due to a breakdown of supply and demand but rather reflects how and where the industry adjusts to sinking demand.

In shrinking corrugated markets, the first response is rarely aggressive price competition. Instead, it’s exit. High-cost mills and inefficient box plants shut first, a pattern that has played out repeatedly over the past two years. As marginal producers disappear, capacity comes out faster than demand, leaving a smaller industry with fewer participants,

more discipline, and less appetite for volume-driven price wars.

Yet discussions of “capacity” often focus on mills. Converting capacity has expanded significantly over the past several years, driven by investment in next-generation corrugators and high-speed boxmaking equipment. When demand softens and buyers test the market, excess converting capacity can exert downward pressure on box pricing—even if containerboard prices remain stable. Plants built on promised return thresholds can’t sit idle indefinitely. That dynamic helps explain why box prices eroded last year, despite limited movement in containerboard benchmarks.

The distinction between containerboard and boxes is critical. Containerboard functions as a commodity purchased by a limited pool of buyers. Boxes are customized products sold to thousands of end users. Yet, most box contracts remain tied to published containerboard assessments, even though the true “open market” represents only a small share of domestic consumption. With integration approaching 90%, much of what moves between mills and plants never reaches the open market.

Exports provide an outlet for excess tons, but those transactions often don’t factor in to domestic benchmark assessments. That allows capacity to clear without necessarily dragging down published prices.

Containerboard’s benchmark price had been flat since February 2025’s increase, even though underlying open-market transactions softened over the past year and box producers across the U.S. reported sustained pricing pressure. This February’s $20-a-ton decline in the benchmark disrupted major integrated producers’ pricing agenda. It also may reflect box buyers’ resolve to test the market and secure lower prices.

Demand erosion is rarely uniform. The customers that change behavior first are typically those with the most flexibility—buyers that can redesign packaging systems or shift formats without major operational disruption. Amazon, for example, has increased its use of paper mailers while relying less on corrugated boxes.

The customers that remain are constrained by equipment, regulation, qualification requirements, or habit. They may resist price increases, but they can’t easily substitute. The pool of box buyers becomes smaller, but demand is less elastic.

In this environment, producers aren’t pricing to the average customer; they’re pricing to customers who are effectively locked in. For large publicly traded companies, pricing in a declining market becomes about preserving cash flow—protecting margins, servicing debt, funding capital spending, and maintaining dividends.

Public markets reinforce this behavior. Investors want growth, but not at the expense of return on invested capital, free cash flow, or earnings per share. Volume growth that destroys returns is penalized, while controlled expansion—or even modest contraction paired with stable margins—is often rewarded.

Once this framing takes hold, pricing becomes a defensive tool, potentially described as “discipline” or “value over volume.” The message isn’t that demand is strong but that accelerating decline by competing away margins is unacceptable.

At this stage of the cycle, the business shifts from growth to harvesting. The objective is no longer to expand the market but to extract as much value as possible from existing assets while they remain economically relevant. This behavior can appear irrational to customers facing higher prices amid weakening demand, but it often makes sense from the producer’s perspective.

Substitutes for corrugated packaging exist—returnable plastic containers or alternative packaging formats—but they aren’t yet cheap, scalable, or frictionless. Switching requires capital, operational focus, and internal justification. As long as those frictions remain, the major integrateds retain some pricing power.

This condition isn’t permanent, though. Higher prices eventually force behavioral change, prompting customers to invest in substitutes, redesign packaging systems, or invite regulatory scrutiny. When the break comes, it’s rarely gradual. If volumes fall below what the remaining asset base can support, pricing power evaporates quickly, and the market fractures.

Prices rising in weakening markets signal where an industry sits in its life cycle. Exit comes first. Substitution comes later. Supply and demand still get the final word—they simply take their time.

Ryan Fox is a corrugated market analyst at Green Markets, a Bloomberg company. He can be reached at rfox93@bloomberg.net.