July 7, 2022

For many years, I have been urging converters to break with the conventional wisdom of full absorption costing, but without it many of you seem lost. Pricing based upon some concept of return on sale (ROS) seems deeply ingrained in your business DNA, and even though you know in your heart of hearts that it doesn’t really work, you desperately cling to it. Your current system may be a “black box” created by someone else based upon a mysterious but supposedly rational system, but you are hesitant to give it up until you find something that makes sense to you.

The answer to this problem is really quite simple and straightforward. Conventional absorption accounting is geared to calculating contribution margin and ROS. Using the concepts of throughput and velocity, as I’ve discussed in many previous articles, requires adding the dimension of time to this equation. The key here are the methodology used to calculate throughput or contribution, and how can you best measure time/velocity, without completely scrapping your existing system? All of you have a system that creates specs, orders, invoices, etc. Your people know how to use these systems, and it would be costly and disruptive to try to replace them. My recommendation is to use the existing systems but with an alternative simplified business model that is based upon hours.

Conventional cost models start with the following:

- Expense budget for the following year stratified by fixed, semifixed, and variable costs.

- Expected footage to be converted at each machine center.

- Other information used for allocations, such as:

- Square footage occupied by the machine center

- Horsepower of the machine

- Expected crew sizes

- Projected delivery miles and cube utilization

- Expected setup times and run speeds for each piece of equipment

Based upon the above, a machine center rate is calculated, and every order will contain a calculation of materials, charges for other variable costs such as labor, repairs, utilities, supplies, a machine center charge, a delivery charge, an allocation of overhead, and a provision for profit. The system will then calculate the expected contribution from the sale and the expected ROS. The worksheets and various other calculations that underly all of this are complicated and cumbersome and often very hard to discern. The theory is that each order must absorb a portion of the company’s overhead. As long as the expected expenses are the same as or lower than the budgeted expenses and the projected volume is higher than the expected volume, this type of system should always produce a profit. This of course assumes that you can make every sale at the desired ROS, which, in point of fact, is rarely the case. If you are going to use this type of system, you must look at the material and labor variances in each job and the total budget variance and the total volume variance that will invariably occur at the company level each month. By looking at these variances and adjusting the model and the efficiency of each order, you can ultimately achieve a well-functioning system.

In practice, almost no one looks at these variances on a regular basis and adjusts the machine efficiencies on each order or the expense and volume budgets that are fundamental to the system. So, what you end up with is finding ways to “trick” your system to come up with what you think are competitive prices that will generate profits for you.

A better approach would be to model your company based upon projected machine hours that are available for sale and setting a goal for the contribution dollars per hour. You can define contribution (sales less variable costs) any way that you think makes sense within your operating methodology. I like to use throughput dollars, which treats materials and commissions as the only true variable costs of the order. My only admonition here is that you reconcile the contribution dollars that the estimating system calculates to the contribution dollars on your actual financial statements. If the numbers are reasonably close and the estimating system is calculating lower contribution than the actual contribution on the financial statements, then in my opinion, you have a very functional system.

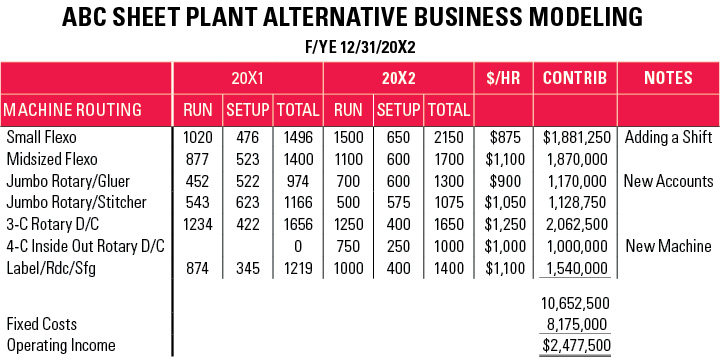

The entire planning process can look something like the table above. You set a target for contribution dollars per hour that each order occupies the machine center (for run and setup) and use this target to evaluate each order. What you will find is that it becomes easy to see which orders are below your standards, and it enables you to take quick action to improve them or decide not to run them. The focus then becomes creating more uptime at each machine center, and calculating the effect of each new piece of business can be quickly evaluated through this lens of dollars per hour. The effect of faster setup times and faster run speeds will be easy to monetize, and you can begin to integrate your plant results and goals into your financial statements.

No matter what ERP system you utilize, this type of alternative business modeling is easily achievable and will allow you to finally understand what effect each order has on the company’s bottom line, without the need for complicated allocations and the determination of what expenses each order has to absorb in order for you to make the desired profits. More machine hours to sell and a higher sales price per hour become the new focus for your business.

Mitch Klingher is a partner at Klingher Nadler LLP. He can be reached at 201-731-3025 or mitch@klinghernadler.com.