March 12, 2026

Box producers appear likely to pursue price increases that outpace input-cost inflation in 2026, and Green Markets wouldn’t be surprised by an attempted move of $50 to $70 a ton. The question is: How will it be implemented?

Many buyers and sellers have said the industry’s benchmark publication failed to reflect pricing realities during a persistently soft 2025. For producers, volatility creates opportunity. When prices move in either direction, it prompts buyers to revisit contracts, test the market, and seek competitive quotes, giving some boxmakers greater leverage as the status quo becomes harder to defend.

Green Markets doesn’t provide price forecasts but rather relies on data to provide grounded analysis of how the market is functioning. This report traces historical containerboard pricing trends, contextualizes recent movements, and outlines what appears to be ahead. We’ll examine cost inputs, supply-demand imbalances, mill closures, and global trade shifts and how those forces may shape pricing strategies in a climate of uncertainty.

We believe any price increase in 2026 would be aimed primarily at halting the erosion in box pricing amid sustained demand weakness. That pressure became more pronounced in the second half of 2025 and was enough to unsettle sheet pricing, particularly for truckload volumes of a single size. Sheet plants, which account for roughly 20% of industry shipments and typically serve lower-volume, more customized orders, reported increasingly inconsistent pricing, a sign of the market’s fragility.

Yet what stood out most was that more containerboard buyers didn’t report lower prices. Few buyers—even those squeezed by downstream price pressure—appeared to be asking their paper suppliers for relief or shopping the market more aggressively. When asked why, one said only that “it’s not the mill’s problem.” Others said they were reluctant to push on price given memories of quotas or supply issues during the COVID-19 pandemic.

Justifying the Price Lift

The next round of price-increase justifications will likely lean less on operating rates and more on structural cost pressures. Rising energy costs, health insurance premiums, wage inflation, and capital equipment expenses should take center stage.

Electric transmission costs have surged in some regions amid the rapid expansion of U.S. data centers, electrical vehicle use, and renewable energy installations. As utilities modernize an aging grid, those infrastructure investments are increasingly being passed on to industrial users. Health insurance premiums also have jumped, with some businesses reporting 30% increases following recent changes to Affordable Care Act funding under the Trump administration.

Labor remains a key cost driver, as well. Retaining skilled workers has become more expensive, with real hourly wages for corrugated box plant employees rising nearly 50% over the past five years. Tariffs continue to fuel price inflation for corrugated machinery and spare parts, further straining capital budgets.

Despite rising costs and softening demand, third-quarter results from publicly traded producers showed margin expansion across the board. International Paper reported an EBITDA (earnings before interest, taxes, depreciation, and amortization) margin of 17.5% through Q3 2025, up 660 basis points from 10.9% a year earlier. Smurfit Westrock’s North American EBITDA margin of 17.2% was slightly ahead of 16.8% a year earlier. Packaging Corp. of America’s year-to-date EBITDA margin was 22.4%, up from 20.5% in 2024.

Though falling shipments remain a concern, improved margins suggest that price realizations from the Q1 2025 increase—combined with cost control—provided a meaningful offset.

Taking the Fun Out of Fundamentals

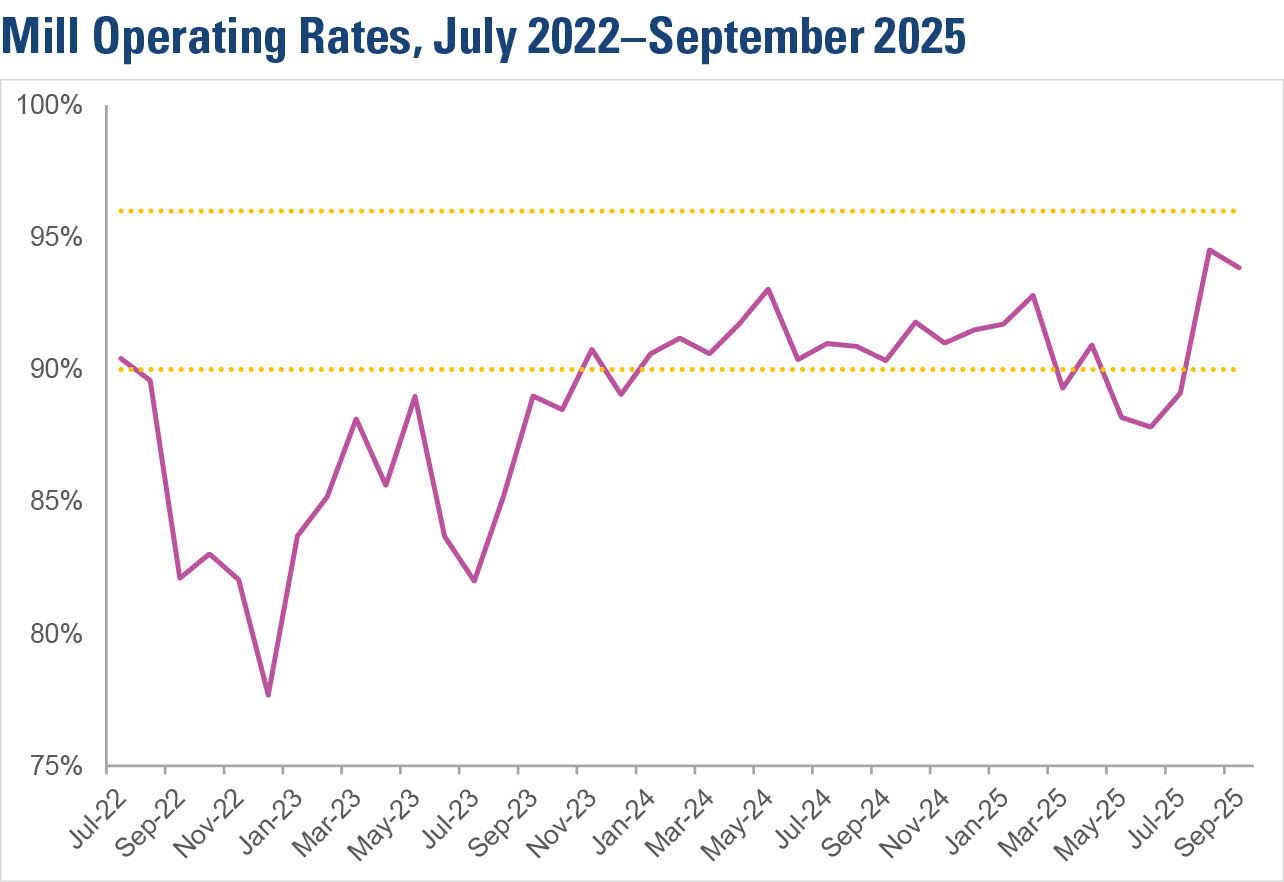

For years, containerboard pricing followed a reliable playbook: Mill operating rates and inventory levels set the tone. When operating rates topped 96%, producers typically had enough pricing power to push through increases. If inventories dipped below 3.5 weeks, a hike often followed. Conversely, when operating rates slipped below 90%, or inventories rose above 4.4 weeks, prices tended to soften. These fundamentals offered a level of predictability that box buyers and sellers alike could use to navigate the market.

In recent years, those fundamentals have lost their predictive power. Mill operating rates have hovered just above 90% for much of the past two years.

When they’ve climbed higher, it’s often due to mill closures or a surge in exports rather than a true demand recovery. In Q3 2025, rates briefly reached 94%, but skepticism lingers. If they top 96% again, will box buyers see that as a genuine sign of tightness or push back, arguing that the number is more the result of supply manipulation?

The elephant in the room is global overcapacity. Numera Analytics reported a global operating rate of just 77% through Q3—a clear sign of excess supply outside North America. Though U.S. tariffs may temporarily limit imports, they also risk constraining exports to Canada and Mexico. Some Canadian producers have already indicated a preference for offshore containerboard, citing both economic and political headwinds tied to U.S. supply.

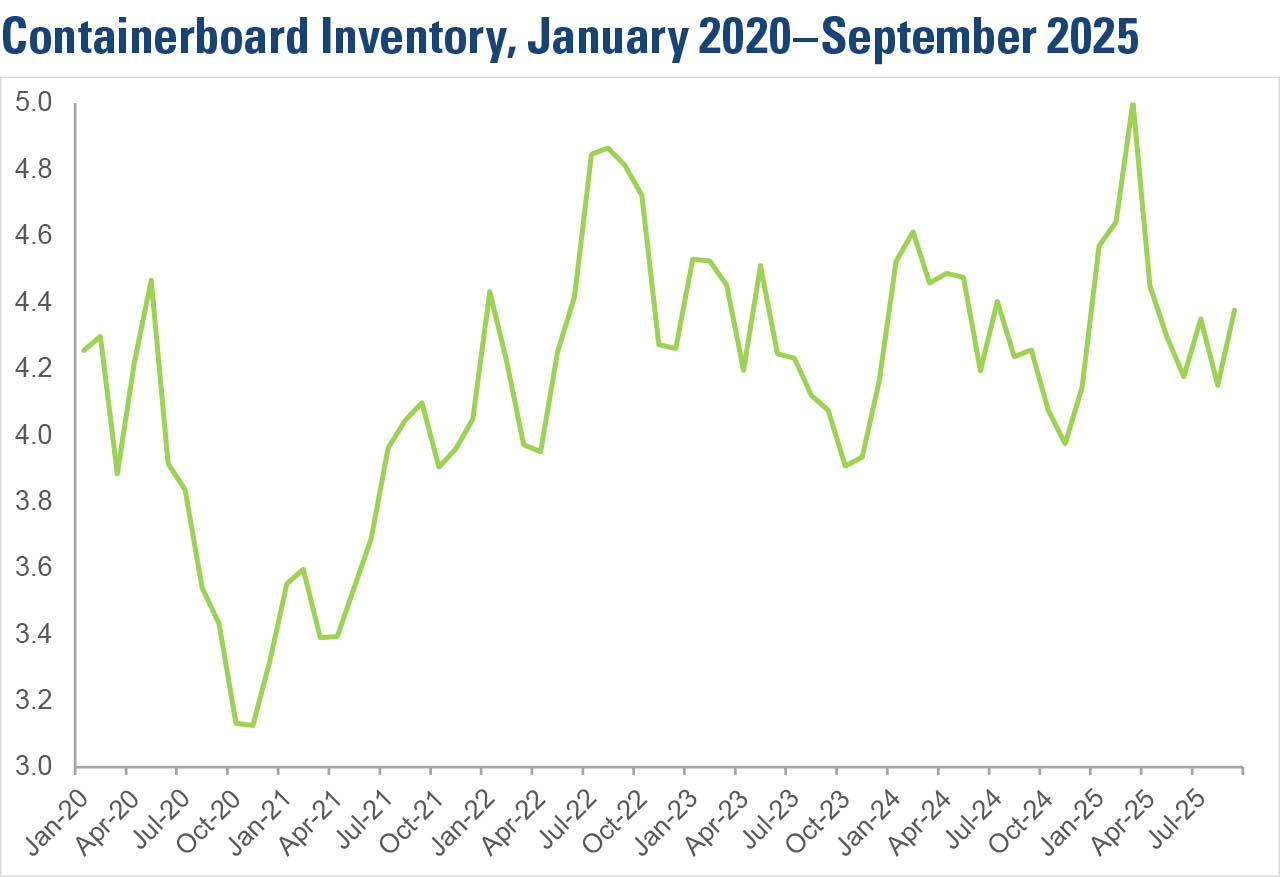

Historically, containerboard inventories served as a reliable indicator of price direction. In mid-2020, inventories rose to 4.5 weeks of supply at the onset of COVID-19. They fell below four weeks by August as product demand surged, bottoming at 3.1 weeks in October and November as mills struggled to keep pace. Costly upgrades and material substitutions followed, and the industry implemented multiple price hikes over an 18-month period.

Post-COVID, as demand softened, inventories climbed, reaching a high of five weeks in March. Yet despite rising stock levels, producers implemented a benchmark-recognized price increase in February 2025. With both inventory and price moving higher simultaneously, the once stable relationship between the two began to break down.

Ryan Fox is a corrugated market analyst at Green Markets, a Bloomberg company. He can be reached at rfox93@bloomberg.