Integrated paper companies such as International Paper, Smurfit Westrock, and Greif own about half of the roughly 70 sheet feeders in the U.S. and Canada, gaining another outlet for their containerboard and allowing them to remove sheets from the mix of full-line box plants, with Pratt being the exception. The remainder are closely held such as those of Corrugated Supplies or co-owned by sheet plants such as Corrugated Partners Group.

In the past five years, some companies such as Greif have sought to bridge the gap between integrated mills and independent box plants. Independent producers have sometimes lost customers to poaching by the same integrated companies that sold them sheets. Greif, which previously lacked converting capabilities, now has seven sheet feeders that offer the normal array of sheets, along with added triple-wall capabilities at plants in Dallas as well as Louisville, Kentucky. The company also owns a sheet plant in Greensboro, North Carolina.

Welch Packaging, based in Elkhart, Indiana, has opened sheet feeders to supply its sheet plants, profiting from integration while expanding through acquisitions, most recently adding SOKY Pack & Pallet of Glasgow, Kentucky. The newest sheet feeder in the U.S., DerbyCorr, is set to come online in the second quarter in Jeffersonville, Indiana, across the river from Louisville.

In a vertically integrated ownership structure, opinions may conflict about what selling prices should be or where profit should be reported. Consortiums bring their own challenges, given that the partners in the sheet feeder may be competitors. Differing motivations or philosophies can affect the long-term success of the business.

In some cases, paper producers have become partners in sheet feeders, perhaps limiting the inclination to source containerboard as cheaply as possible. A strong third-party manager for the sheet feeder can temper the risk of conflicts.

Speed as Part of the Value Segment

Responsiveness, defined as lead time to deliver an order, is key for companies that want to add value and charge customers a premium. For corrugated producers, it’s perhaps the most common way to capitalize on value over volume. The speed provided by sheet feeders has helped to fuel the market share growth of sheet plants.

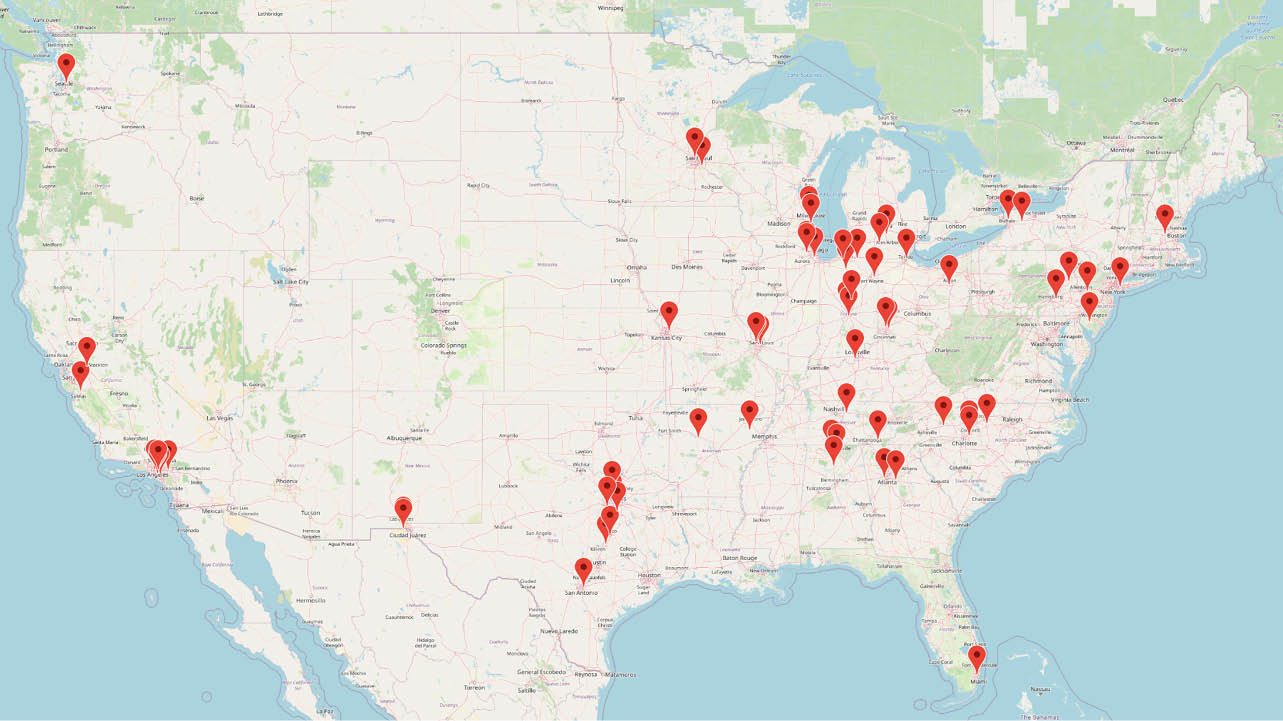

View of sheet feeders throughout the United States. (Source: Fibre Box Association.)

Lead times for full-line box plants traditionally range from two days to three weeks depending on general market conditions. During the COVID-19 pandemic’s demand peak, on-time performance suffered: Lead times of four to six weeks weren’t uncommon, and some stretched as long as 10 to 12 weeks.

Full-line box plants that sell to high-volume segments of the market strive for maximum efficiency, often limiting flute changes or running some grades only on certain days of the week. By contrast, sheet feeders might make multiple flute changes daily to meet short lead-time commitments to customers.

Unlike full-line plants, sheet feeders typically operate without a large backlog, perhaps one to three days, as they strive to flush orders through the system quickly. This allows sheet plants to put raw material behind their converting equipment in 24 to 48 hours, much faster than a typical full-line plant, and deliver a finished product in less than a week. Some sheet plants manage inventory for customers and have replenishment orders ready in the system that can be moved out to accommodate a customer’s request for a fast response.

Ryan Fox is a corrugated market analyst at Green Markets, a Bloomberg company.